What percentage of your sites are you converting to RRH (remote radio head) technology?

RRH technology takes radios that typically have been at ground level and places them on the towers behind the antennas. The RRH technology is useful in providing better coverage for the higher frequency spectrum. For AT&T, RRH technology would help mitigate the coverage differential between 700MHz and PCS, 700MHz and AWS, and 700MHz and WCS. If low band coverage (700MHz) were represented by a quarter, and mid band coverage (PCS) by a dime; moving the PCS channel to RRH technology would make the PCS coverage grow to the size of a nickel. This would allow AT&T to have similar capacity across a larger amount of their coverage.

Are you using RRH technology only for your high band spectrum or all spectrum except low band?

Applying RRH technology to low band spectrum in rural areas would fill in coverage holes but increasing coverage in urban areas with RRH technology would increase interference.

What percentage of your customers have a device that will operate on 700 MHz (band 17), AWS (band 4), and WCS (band 30)?

The iPhone 6s has an available version that supports the WCS band, but since not all of AT&T’s customers have a phone that supports their entire LTE spectrum, network coverage and capacity enhancements will not be experienced by the entire user base.

How much back haul capacity do you provide to each cell site for each 10 MHz of LTE spectrum?

To prevent back haul from being a bottleneck, 225 Mbps should be provided for each 10 MHz of spectrum (75Mbps per sector).

What is your average monthly back haul cost per cell site ($/Mbps)?

Site back haul costs would surprise many in the analyst community. When sites only supported voice calls, site leases (land and tower) dominated the operations expense. With the move to data, the site lease (average $1500/mo) is dominated by the back haul lease ($8000/mo). This becomes more painful as you consider the need for doubling data capacity which could then double your site back haul expense.

The news yesterday that T-Mobile and Sprint are forming a Joint Venture to buy 600MHz Broadcast Incentive Auction spectrum shows a shift in the way that both Sprint and T-Mobile look at the places that aren't in non-Top 100 markets, along Interstates, or along US Highway routes.

Will the T-Mobile/Sprint JV use this low band spectrum to fill out the areas that they rely on partners (primarly AT&T and Sprint) to provide their coverage? Virtually all of T-Mobile's recently acquired 700MHz A band spectrum is in large cities (see my post from 11/2013) and Sprint has been reluctant to add towers in rural areas to utilized the 7MHz of low band SMR spectrum that they are using elsewhere for their Spark service.

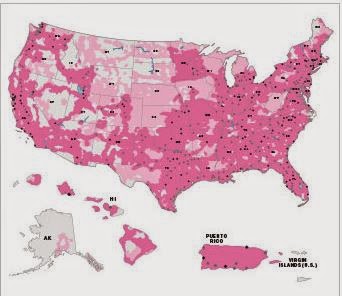

Sprint's Current Coverage

T-Mobile Coverage (Light Pink indicates Partner Coverage)

T-Mobile has signaled with the FCC that they are concerned about reasonable roaming rates and Sprint is clearly in the same position with Verizon, needing Verizon's coverage to offer true nationwide coverage. On the other side of the coin, T-Mobile indicates that they already cover 96% of the US population, leaving about 12.5 million POPs to be covered with this new low band spectrum.

For both T-Mobile and Sprint a build out in these uncovered areas would reduce their risk of of significant rate increases or roaming service elimination with Verizon and AT&T, but these towers would be much less efficient than towers elsewhere in their collective networks. Obviously they would share the deployment costs and operating cost, but with these towers would have serve a low number of POPS (population)/Tower which is a standard industry metric on capital efficiency for deployed towers.

How would this affect Sprint's recent regional partners?Sprint Regional PartnersBuilding out this spectrum would put Sprint in direct competition with these recent formed partners. These regional partners may also participate in the auction acquiring more spectrum. Each of these partners only needs low band spectrum for wide area coverage, and there are ample amounts of mid-band (PCS/AWS) spectrum in these areas for these regional partners to uses as capacity grows.

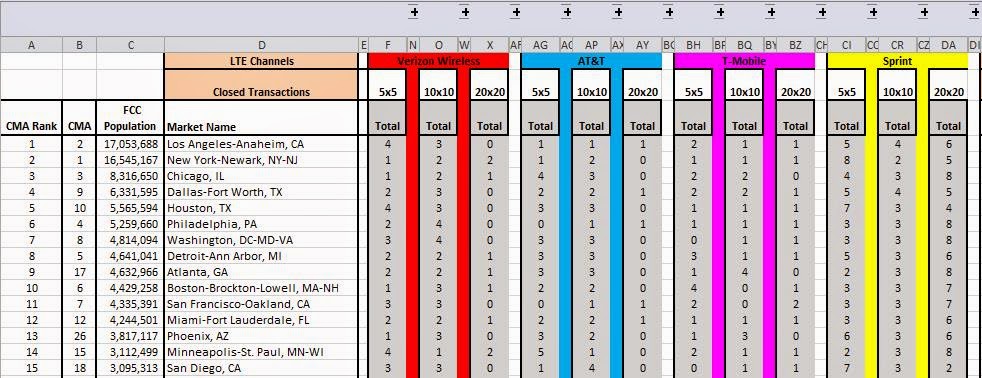

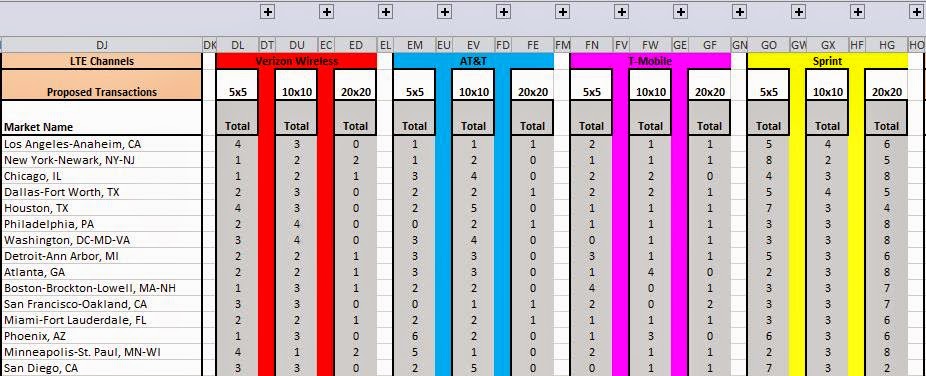

AllNet Labs is now offering a monthly spectrum report summarizing the LTE Channels for the National Carriers (Verizon, AT&T, Sprint, and T-Mobile). To develop this report, AllNet Labs takes the spectrum outputs at a county level from its Spectrum Analysis Tool and applies a county population weighting before averaging all of the counties within a Cellular Market Area (CMA). Data is available for all 733 CMA markets, but the standard report is formatted for the 100 most populated CMA markets. This report is delivered as an Excel spreadsheet, with both summary and detailed views. In the summary view (Figure 1), only the size and quantity of LTE channels for each carrier are displayed. This report evaluates each carrier’s complete spectrum holdings to determine the size and quantity of available LTE channels. The report also assumes that the largest channel would be utilized rather than multiple smaller channels (e.g. a 20MHz channel is assumed rather than 2 – 10MHz channels).

|

| Figure 1 |

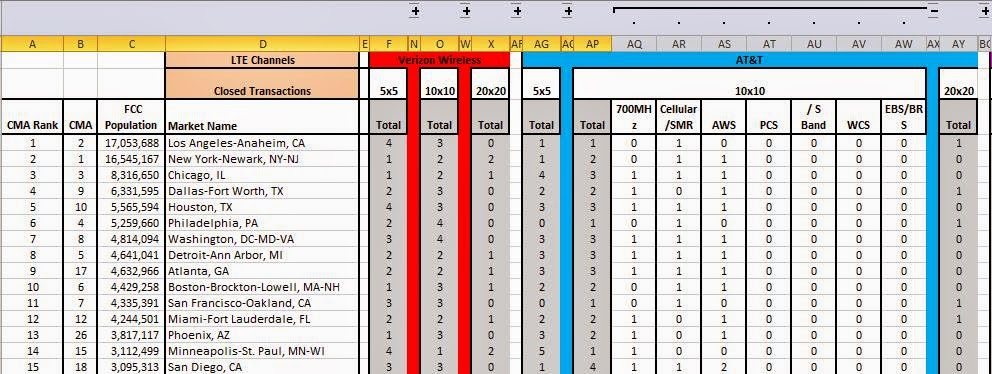

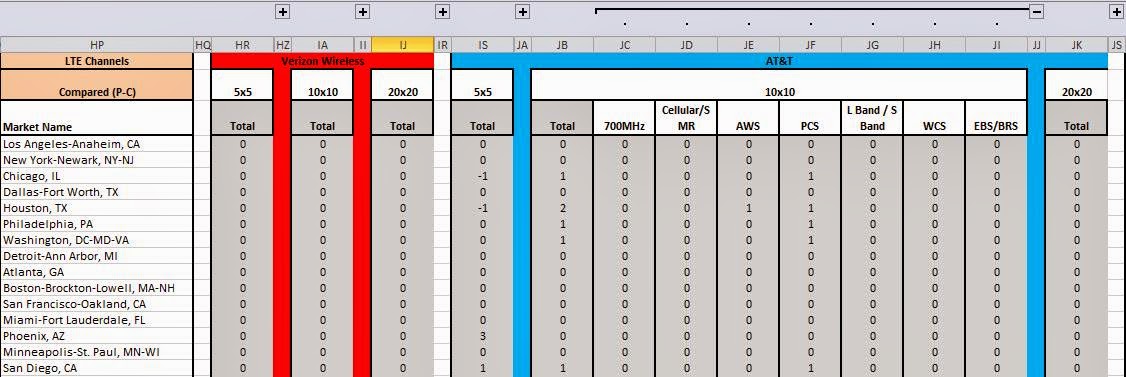

By selecting the [+] in the upper margin to the right of AT&T’s 10x10 column we can reveal t AT&T’s LTE channel distribution by band. This expanded view is seen below as Figure 2.  |

| Figure 2 |

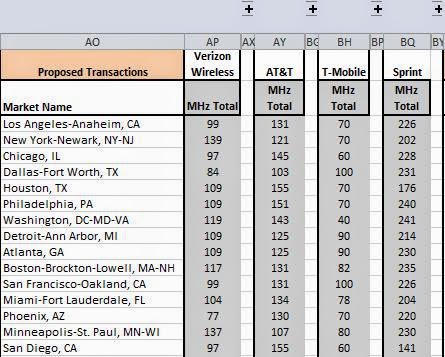

AllNet Labs has added a proposed transaction data set to the Spectrum Analysis Tool. With this data set, we are able to simplify hundreds of license transfers at the FCC into the net effect for wireless operators. All of the transactions are captured from the FCC Daily Digest and each license is updated at the callsign, county, and frequency levels. Using this proposed transaction data; a matrix of each carrier’s future LTE Channels is created (Figure 3).  |

| Figure 3 |

By selecting the [+] signs in the upper margin, a carrier’s spectrum holdings by band can be detailed. (Figure 4). |

| Figure 4 |

The last matrix in this report summarizes the differences between the proposed LTE Channels and the current LTE Channels. This highlights areas that are affected by proposed transactions. The example shown uses data from the December 2013 Spectrum Analysis Tool. The proposed transactions for December 2013 were transactions announced prior to 12/1 which included AT&T’s purchase of Leap as well as many other minor transactions. The effect of that transaction as well as other more minor transactions is easily seen in Figure 5, with AT&T increasing their LTE channel size from 5x5 to 10x10 in Chicago. |

| Figure 5 |

To see the changes at the spectrum band level of detail, select the [+] in the upper margin as described before. As seen in Figure 6, AT&T’s increase in 10x10 channels in Chicago was the result of an increase in the PCS spectrum band.

|

| Figure 6 |

AllNet Lab's Spectrum Analysis Tool is an Excel based product which allows users to visualize and analyze the current spectrum ownership for all of the mobile carrier and satellite frequency bands at a county level for all 50 states and US territories. The Spectrum Analysis Tool includes 15 color-coded spectrum holders and over 600 additional identified carriers. More information can be found at www.allnetlabs.com.

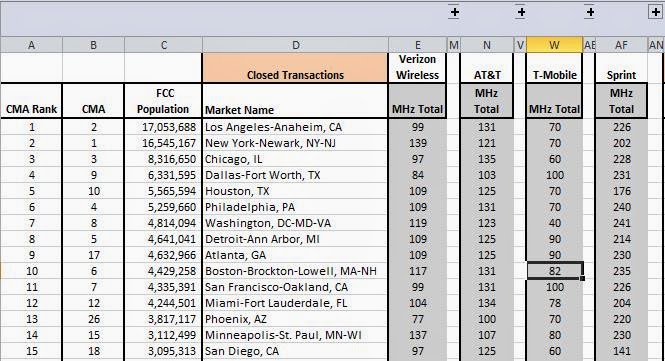

AllNet Labs is now offering a monthly spectrum report summarizing the spectrum holdings for the National Carriers (Verizon, AT&T, Sprint, and T-Mobile). To develop this report, AllNet Labs takes the spectrum outputs at a county level from its Spectrum Analysis Tooland applies a county population weighting before averaging all of the counties within a Cellular Market Area (CMA). Data is available for all 733 CMA markets, but the standard report is formatted for the 100 most populated CMA markets. This report is delivered as an Excel spreadsheet, with both summary and detailed views. In the summary view (Figure 1), only the total spectrum holdings for each carrier are displayed. |

| Figure 1 |

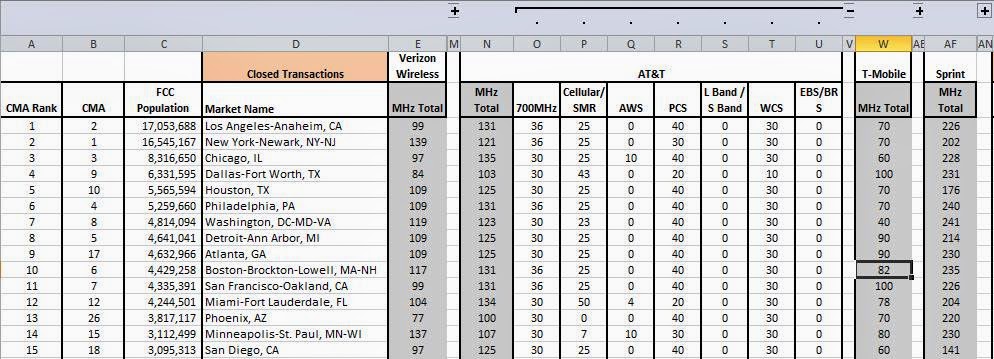

By selecting the [+] in the upper margin to the right of AT&T spectrum holdings we can reveal AT&T’s spectrum distribution by band. This expanded view is seen below as Figure 2. |

| Figure 2 |

AllNet Labs has added a proposed transaction data set to the Spectrum Analysis Tool. With this data set, we are able to simplify hundreds of license transfers at the FCC into the net effect for wireless operators. All of the transactions are captured from the FCC Daily Digest and each license is updated at the callsign, county, and frequency levels. Using this proposed transaction data, a matrix of the national carrier’s proposed spectrum holdings is created (Figure 3).  |

| Figure 3 |

By selecting the [+] signs in the upper margin, a carrier’s spectrum holdings by band can be detailed. (Figure 4). |

| Figure 4 |

The last matrix in this report summarizes the differences between the proposed spectrum holdings and the current spectrum holdings. This highlights areas that are affected by proposed transactions. The example shown uses data from the December 2013 Spectrum Analysis Tool. The proposed transactions for December 2013 were transactions announced prior to 12/1 which included AT&T’s purchase of Leap as well as many other minor transactions. The effect of that transaction as well as other more minor transactions is easily seen in Figure 5, with AT&T increasing their spectrum holdings in 6 of the 15 CMA markets listed. |

| Figure 5 |

To see the changes at the spectrum band level of detail, select the [+] in the upper margin as described before. As seen in Figure 6, AT&T’s increase in spectrum was the result of increases in AWS and PCS spectrum, which matches the known spectrum that Leap will bring to AT&T. |

| Figure 6 |

AllNet Lab's Spectrum Analysis Tool is an Excel based product which allows users to visualize and analyze the current spectrum ownership for all of the mobile carrier and satellite frequency bands at a county level for all 50 states and US territories. The Spectrum Analysis Tool includes 15 color-coded spectrum holders and over 600 additional identified carriers. More information can be found at www.allnetlabs.com.

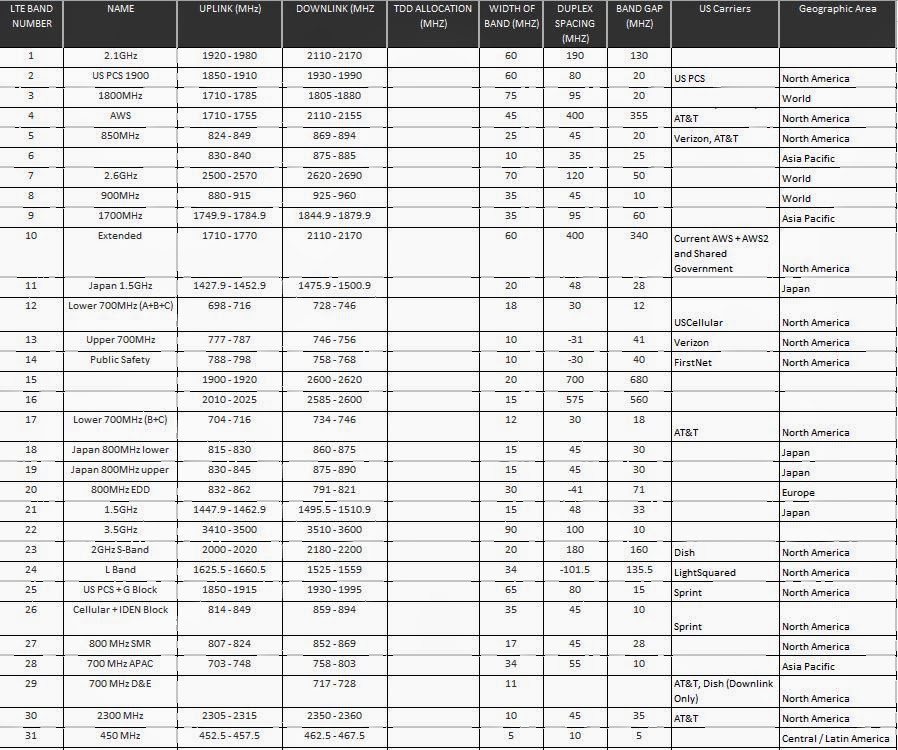

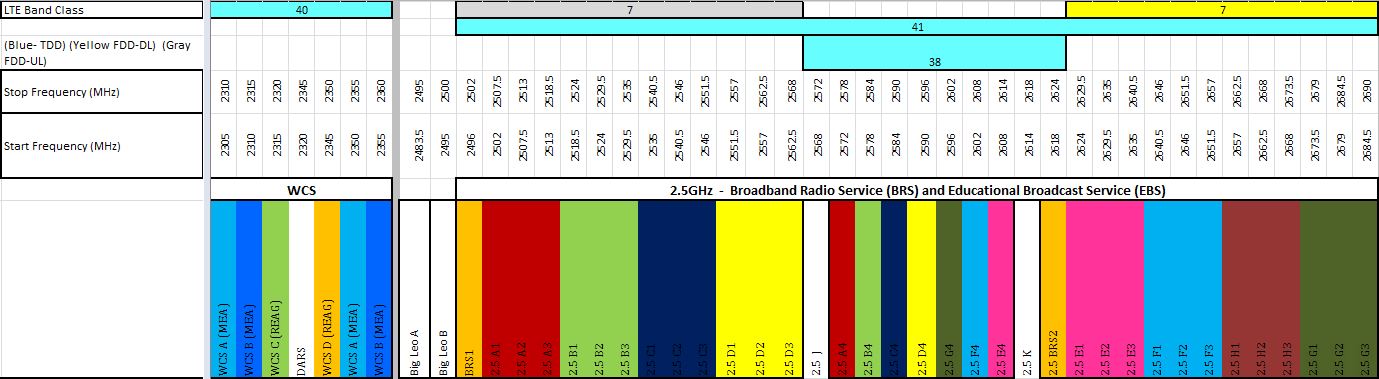

As I was completing my research for an upcoming blog on LTE Carrier Aggregation, I found that my previous LTE Band Class reference sheet was missing some of the more recent Band Class updates, so I decided to share my new reference document with a few comments.

FDD Band Classes:

The first notable band class addition in Band 30. This band class creates a definition for FDD operation in the WCS (2.3GHz) band which was previously defined only for TDD operation.

From the Spectrum Grid view of the Spectrum Ownership and Analysis Tool, you can see that Band 30 does not include the 5MHz channels that AT&T purchased to essentially become guard bands for the Satellite Audio guys. This will provide AT&T with a 10x10 LTE channel on a market by market basis, as they resolve the remaining ownership issues in the WCS band.

The next two band classes are not new, but I previously skipped over these band classes because I didn't fully understand their frequency breaks.

Band 26Previously I thought this was a specific band for Sprint IDEN operation that is adjacent to the cellular band. This is the band where Sprint is placing their 2nd LTE channel (5 MHz) and a CDMA channel (1.23 MHz). Looking at the frequencies in detail, the band class covers the IDEN spectrum and the adjacent cellular spectrum.

This is similar to Sprint's Band 25 which includes all of the PCS band plus their G block spectrum (but not the H block).

So you would think that all of the North American carriers could standardize to Band 25 for PCS operation and Band 26 for Cellular. Using the latest iPhone 5s LTE band support,

you can see the Verizon, T-Mobile, and AT&T iPhone's support Band 2 and 25 for PCS, but only the cellular band (Band 5). Sprint iPhone 5s includes,

both Band 2 and 25 for PCS and Band 5 and 26 for cellular.

Band 10:

This is referenced as the AWS extended band and you can note from above that it is not currently applied to smartphones like the iPhone 5s. This band class seems to be a preparation for the future use of the AWS-2 and AWS-3 spectrum and the government shared use band that are both adjacent to the existing AWS spectrum band. Here is how the downlink looks in the Spectrum Ownership Analysis Tool:

Note that Band 10 does not cover the entire band contemplated for AWS-3, nor does it include Dish's Band 23. For the uplink:

This again depicts that Band 10 is not currently set to include the entire shared government opportunity.

TDD Band Classes:

Here is the reference sheet the TDD band classes.

On this reference sheet I hadn't looked closely at band classes 35, 36, and 37. I had always focused on the 2.3GHz and 2.5GHz as the only bands that were designated for TDD support in North America. These three band classes create 140MHz block of spectrum that could be for TDD deployment. Here is how these bands appear in the Spectrum Ownership Analysis Tool:

I'm not sure what the history is on these band classes, but they would support TDD operation in both the PCS uplink and downlink bands as well as in the 20 MHz between the bands. Since the PCS frequencies are highly deployed, I would consider it very unlikely to see TDD systems in this band in the near future, and I doubt that the PCS band is authorized for TDD operation. It will be interesting to see whether any of the wireless carriers begin to look this direction. With Sprint stepping out of the H block auction, they seem to be signalling that TDD operation is more important to them and the Band 37 block (including Sprint's G block) could be the reason why Dish is pushing forward in the H block auction. Please comment if you are aware why the 3GPP has included these 3 TDD band classes.

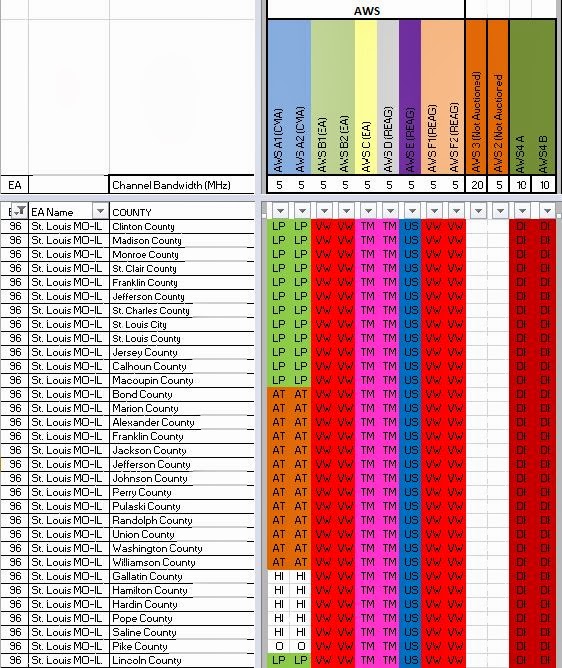

It is interesting to look at the details of Verizon's spectrum purchase from US Cellular in the St Louis market area (EA-96). Many industry sources talk about how purchase will provide 20MHz for Verizon's LTE. While this is true, it should not be confused with Verizon deploying a 20 x 20 channel. As can be seen from the Spectrum Grid view of AllNet Labs' Spectrum Ownership Analysis Tool, Verizon is purchasing the AWS B channel and previously owned the F channel. Although Verizon will own 20 MHz of spectrum, it is not contiguous and until they can deploy Release 12 software code into their network, they will have to operate this spectrum as two separate 10 MHz channels. Release 12 is likely a 2015 or maybe 2016 release since operators are either planning or deploying Release 10 currently.

The industry talks alot about Carrier Aggregation (CA) but there are several facts that are not well understood. First, Release 10 includes the functionality for carrier aggregation but the frequency band definitions for the US are not included until Release 11. Another point that needs to be understood is that the initial definitions require that aggregated carriers be in contiguous blocks in different spectrum bands (inter-band) or in separate blocks but in the same band (intra-band). For Release 11, only 2 carriers can be aggregated together. For Release 12, Verizon has sponsored a work group that will allow 3 carriers to be aggregated, 1 from the 700MHz band and 2 different carriers from the AWS band. Thus, Release 12 will be necessary for Verizon to aggregate their two AWS blocks of spectrum with their 700 MHz LTE.

The Spectrum Grid view is sorted by the EA geographical area which show that the AWS B and C licenses have not be dis-aggregated. The A channel licenses do show discontinuity since they were originally auctioned as CMA licenses. AT&T through their Leap purchase will strengthen their AWS ownership in this market.

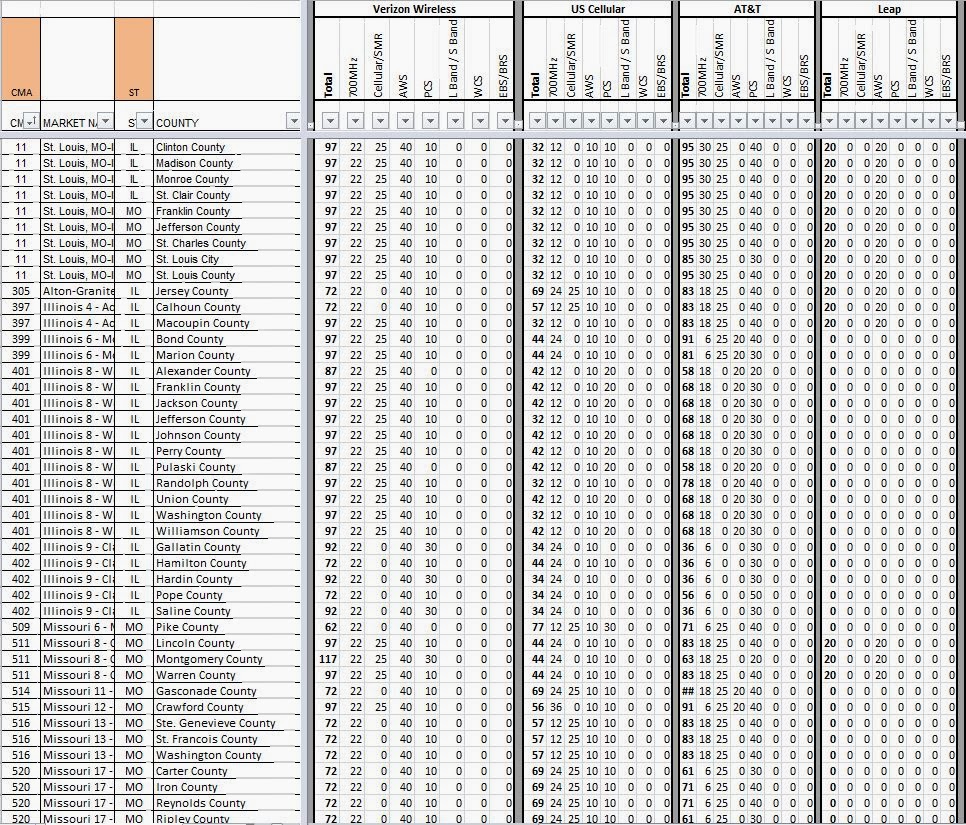

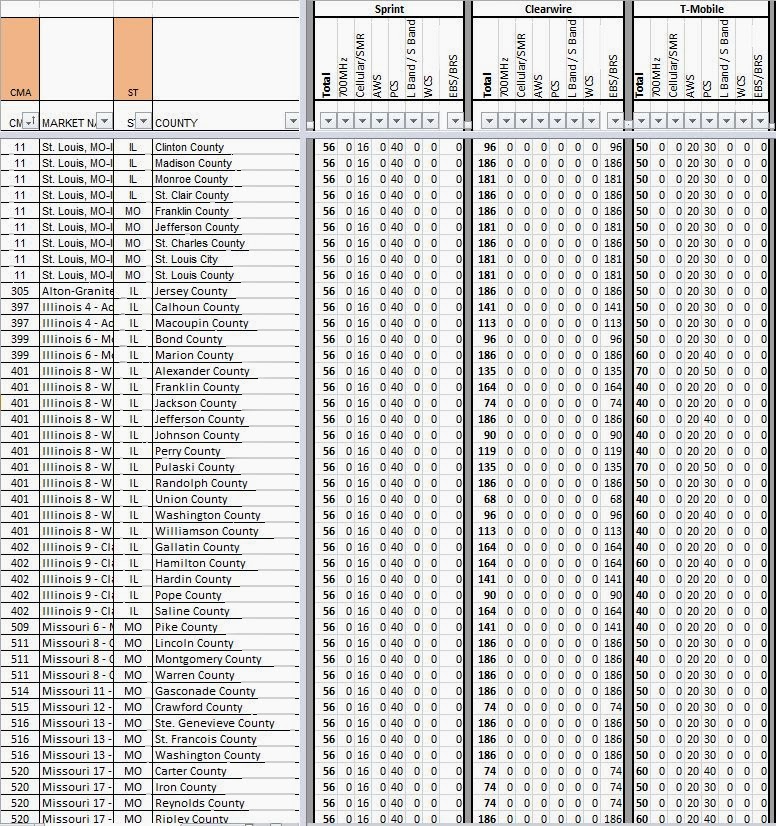

To look at the competitive picture for spectrum in the St Louis market (EA-96) we can look at the

Company By Band worksheet from the AllNet Labs' Spectrum Ownership Analysis Tool. Looking first at Verizon, we can see the variety of spectrum depths across the EA that Verizon indicated in their FCC filing. Verizon will range from 62 MHz to 117 MHz depending on the county. The only county that Verizon controls 117 MHz is Montgomery County, MO which is 40 miles west of St. Louis.

Looking at the other carriers in this market we see that US Cellular will still control between 32 MHz and 69 MHz, while AT&T with their Leap purchase will control between 61 MHz and 105 MHz.

T-Mobile controls between 40 MHz and 60 MHz with two counties at 70 MHz and Sprint with their Clearwire purchase controls between 130 MHz and 242 MHz.

For the past month I have been examining the effect of WiFi off-loading based upon my usage habits. To do this leave WiFi turned off so my phone only receives data service from a commercial carrier network. This was not a simple task because the Smartphone network optimizer will continue to request to have WiFi turned on and whenever you are using location services (Google+) not having WiFi provides a notification "to improve you location, please turn on WiFi".

My typical monthly data usage averages around 1.3 GB per month with WiFi enabled. I travel infrequently and have WiFi both at home and work. I think it is important to note that my work WiFi doesn't block YouTube, Pandora, Facebook, or WatchESPN, but I typically use a WiFi only tablet for music streaming or the watching a major sporting event e.g The America's Cup or the MBL playoffs.

In the month of September, I ran 5.7 GB of data in what I consider to be a typical work month. What this equates to is 3.4 GB of data that was off-loaded from the carrier network to the WiFi network for which I also pay. Another way to look at it is that my carrier only sees 1/3 of my usage.

Using some of the wholesale data rates that have been thrown around in the trade press, $5/GB; the cost to support my data usage through a WiFi Off-loading provider would be $17/month. If I am paying my carrier $30/month for my data usage and they pay a Wi-Fi off-loading provider $17/month, they only end up with $13/month to offset their operational expenses (site leases, backhaul costs, employees...)

When you consider the "true" smartphone usage and where the majority of that traffic is handled today, it is clear why cellular carriers have been reluctant to purchase wholesale access to data or a WiFi off-loading partner.

Check back next month. After my billing period closed, I spent the weekend out of town, so streaming two college football games on Saturday (Dish Anywhere) and 1 NFL game on Sunday will all be part of my October usage. With just 9 days on my billing cycle, I have already consumed 3.3 GB.

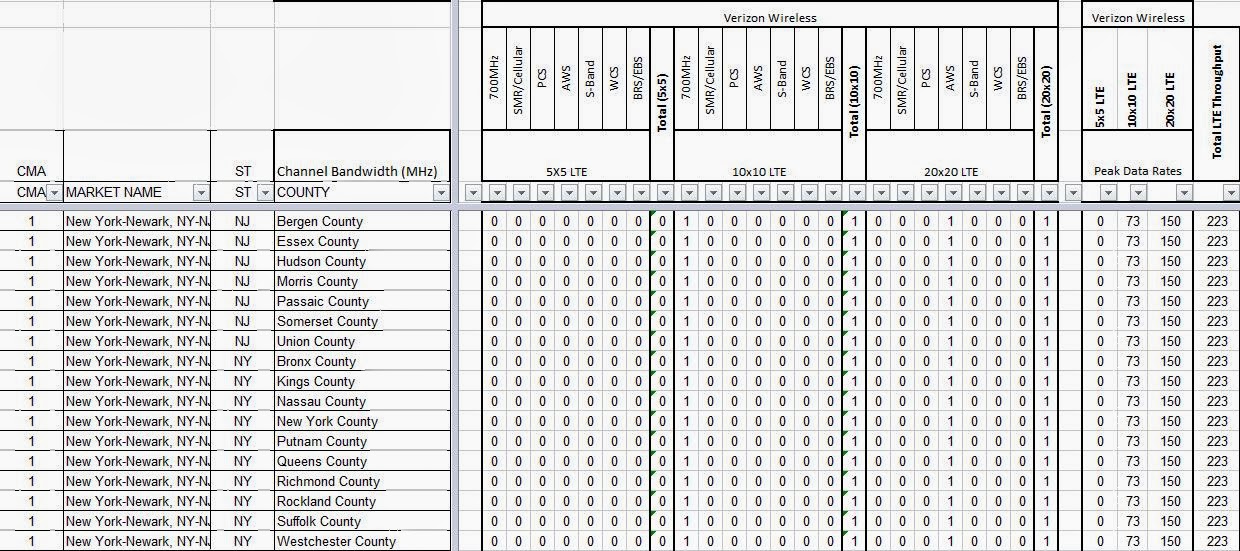

With the news that Verizon is beginning to turn up some of their AWS spectrum with LTE, I will examine the spectrum available for those LTE deployments in the Top 5 CMAs with the Spectrum Ownership Analysis Tool.

New York:

Verizon clearly holds 40 MHz of AWS spectrum. To see how this spectrum will affect their total LTE capacity I have evaluated the LTE channels that Verizon can deploy based on their stated direction. Based upon Verizon's stated direction I have eliminated any 700 MHz 5x5 LTE channels, any cellular LTE channels, and any PCS LTE channels.

With this analysis, it is evident that Verizon will top out at 223 Mbps across all of the counties in the New York CMA.

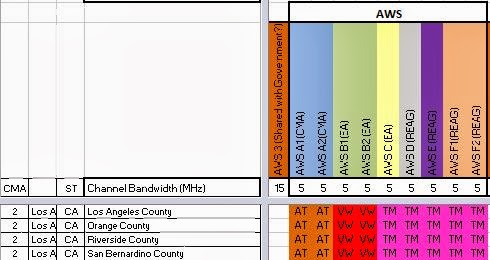

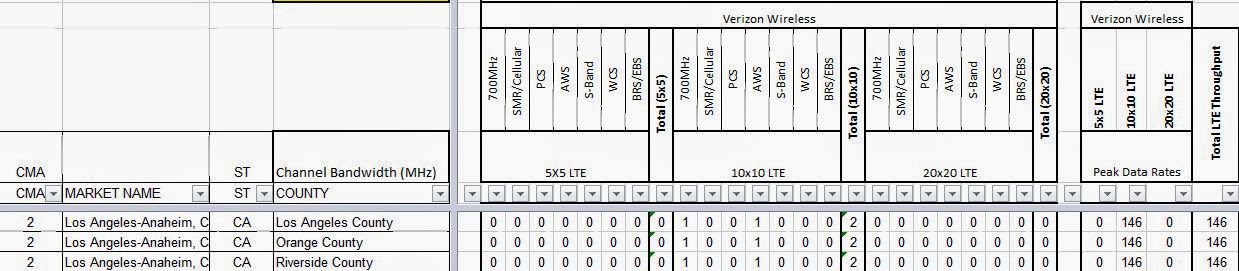

Los Angeles: In Los Angeles, I would expect Verizon to be deploying a 10 MHz LTE channel until AT&T has shifted its LTE usage of this AWS channel to it "new" 700MHz B band holding.

At this point Verizon is limited to 2 - 10x10 channels or 146 Mbps throughout the Los Angeles CMA.

Chicago:In Chicago, Verizon holds a 20x20 AWS channel.

This combined with Verizon's 700 MHz C-band (10x10) channel will provide 223 Mbps throughout the Chicago CMA.

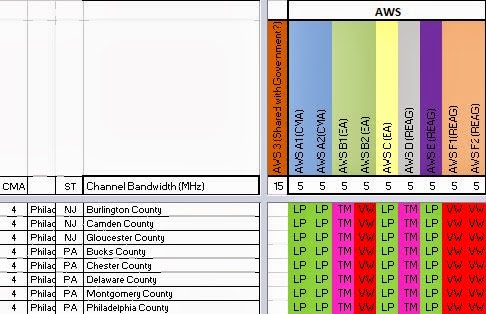

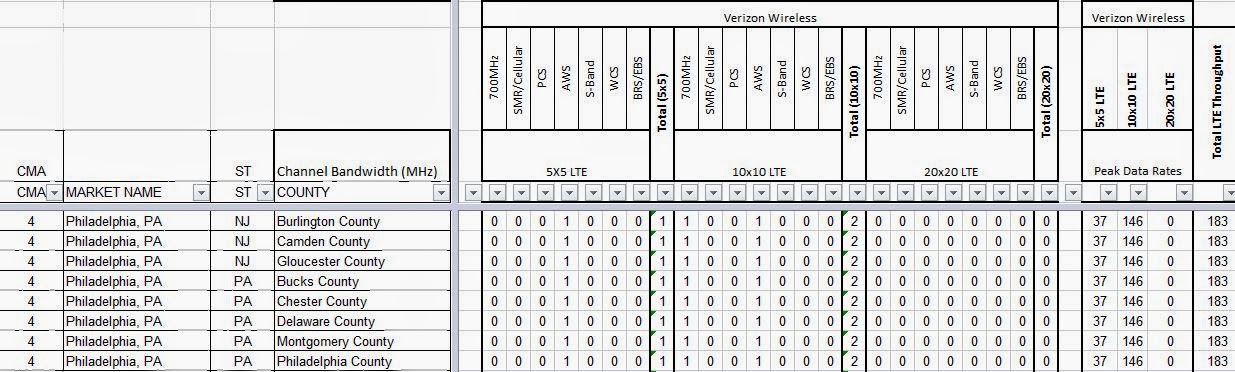

Philadelphia:

In Philadelphia, the largest channel Verizon can form is a 10x10 channel. When AT&T gets control of the Leap spectrum assets, I would expect a three-way spectrum trade to allow Verizon, T-Mobile, and AT&T to rationalize their AWS spectrum positions.

For the throughput analysis, the additional 5x5 channel that Verizon can form in the AWS frequency band is included with the 2 - 10x10 channels (AWS and 700) for a total metro throughput of 183 Mbps.

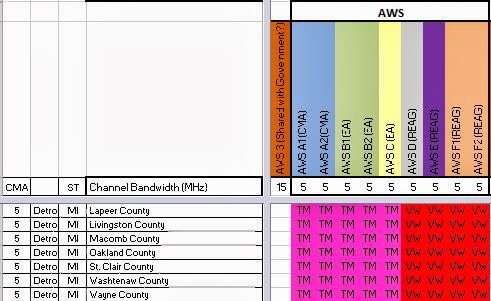

Detroit:In Detroit, Verizon can again form a 20x20 AWS channel.

In the Detroit CMA, Verizon can achieve a metro through put of 223 Mbps.

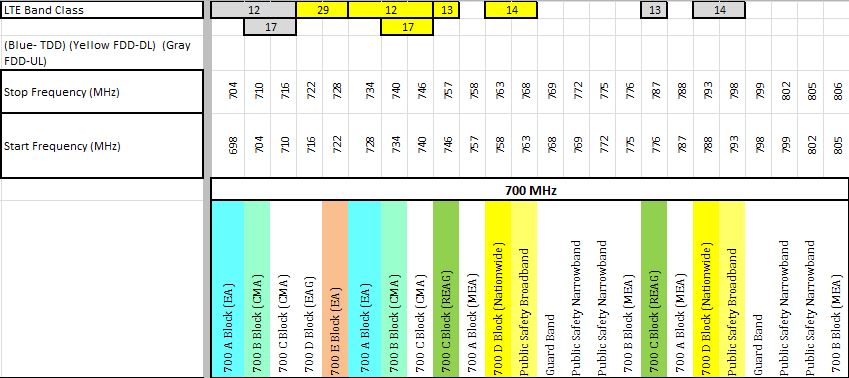

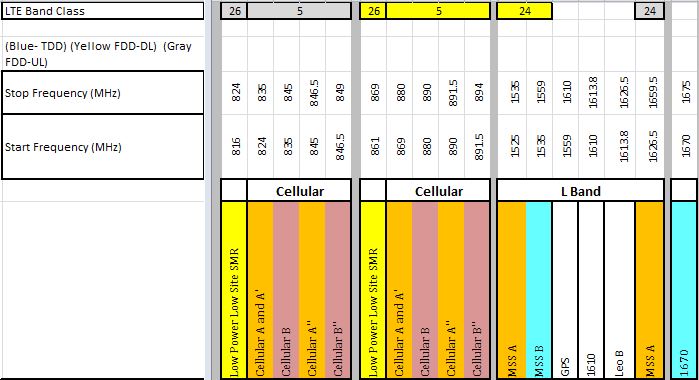

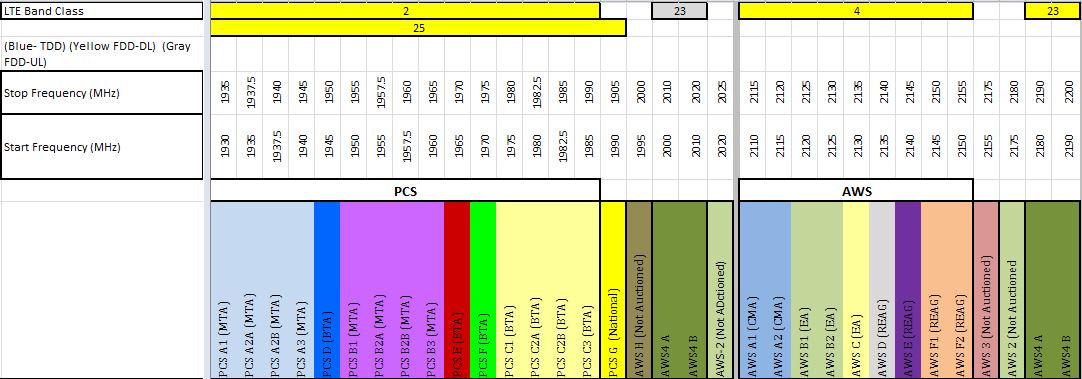

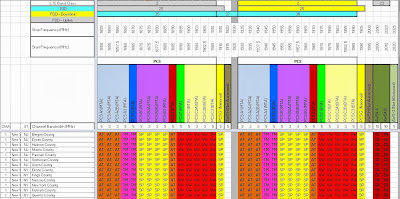

With AT&T's announcement that they are meeting some challenges related to testing operation between LTE Band Class 29 and Band Classes 2 and 4, I figured that many readers would appreciate a reference map for how these band classes relate to the US mobile radio and satellite spectrum bands.

All of these screenshots are from the AllNet Labs Spectrum Ownership Analysis Tool, where we display and provide analysis tools related to spectrum ownership for all of the US mobile radio and satellite spectrum bands for all 50 states and US territories.

AllNet Labs Spectrum Ownership Analysis ToolIn the images below, the band classes are color coded Gray for Uplink Spectrum, Yellow for Downlink Spectrum, and Blue for Spectrum supporting Time Division Duplex.

700MHz Spectrum

SMR/Cellular/L-Band Spectrum

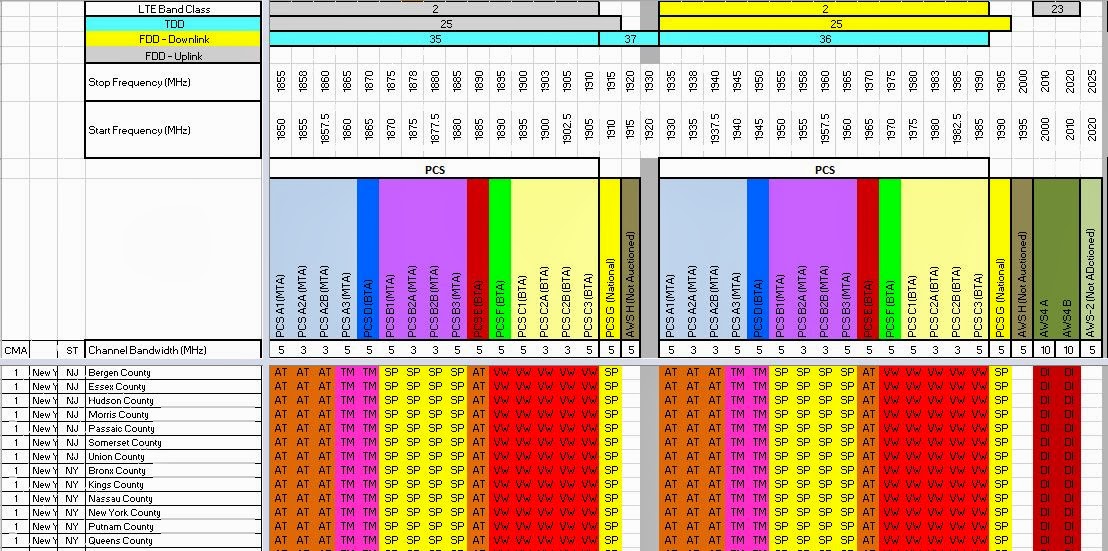

AWS/PCS Spectrum - Uplink

PCS/AWS Spectrum - Downlink

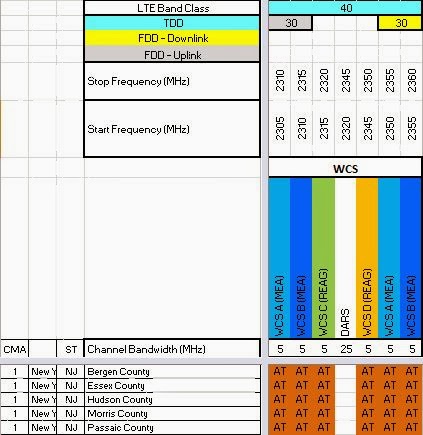

WCS/EBS/BRS Spectrum

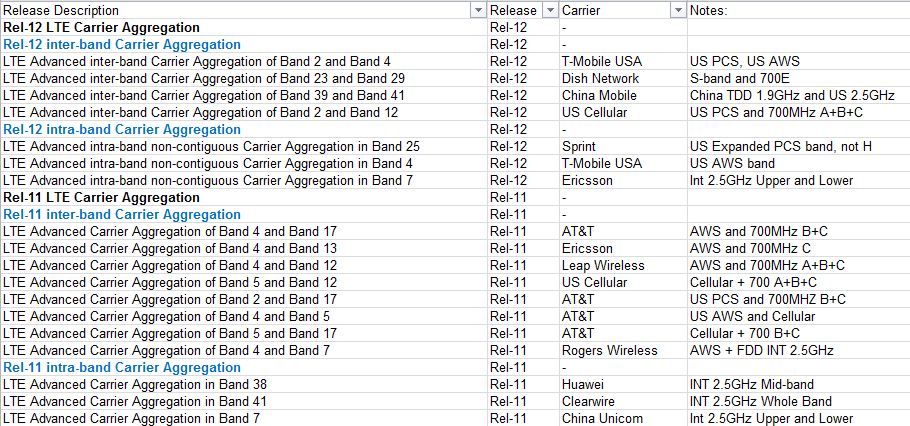

Recently I reviewed the 3GPP Standards site to check in on the status of LTE Carrier Aggregation. I found a gold mine of information.

First a few definitions: Carrier Aggregation allows a wireless carrier to band together different blocks of their spectrum to form a larger pipe for LTE. This can be accomplished in two ways: Inter-band and Intra-band.

Inter-band combines spectrum from two different bands. The spectrum in each band to be combined must be contiguous within that band. Intra-band combines spectrum from two non-contiguous areas of the same band.

Here is a link to an article from 3GPP that explains Carrier Aggregation.Below is a table summarizing the relevant 3GPP working group descriptions for Carrier Aggregation.

First of all, the current network release for all carriers is Release 9. T-Mobile, Sprint, and Clearwire have announced that they are deploying Release 9 equipment that is software up-gradable to Release 10 (LTE Advance). From the chart, it does not appear that there are any carrier configurations planned until Release 11. Release 10 appears to be a late 2013 commercial appearance and Release 11 will likely be very late 2014 or mid-2015. For Carrier Aggregation to work it must be enabled and configured at the cell site base station and a compatible handset must be available. The handsets will transmit and receive their LTE data on two different spectrum bands for the Inter-band solution. All handsets currently only operate in one mode, 700MHz, Cellular, PCS, AWS, or 2.5GHz.

Highlights by Carrier:

Canada: Rogers Wireless will have support for inter-band aggregation between their AWS spectrum and the paired blocks of 2.5GHz spectrum.

AT&T: Inter-band support in Release 11 for their Cellular and 700MHz spectrum, inter-band support to combine their AWS and Cellular spectrum, as well as configuration to support combining their PCS and 700MHz spectrum. All of the 700MHz band plans only include their 700B/C holdings. No 700MHz inter-operability.

USCellular: Inter-band support in Release 11 for Cellular and 700MHz (A/B/C). No support for PCS or AWS spectrum combinations

Clearwire: Intra-band support for the entire 2.5GHz band. China Mobile is also supporting this with an inter-band aggregation between 2.5GHz and their TDD 1.9GHz spectrum.

Sprint: Support in Release 12 for combining (intra-band)their holding across the PCS spectrum, including their G spectrum but not the un-auctioned H spectrum. No band support for their iDEN band or the 2.5GHz band.

T-Mobile: Support in Release 12 for intra-band in the AWS band and inter-band between AWS and PCS.

Verizon: Ericsson appears to be supporting Verizon's need to combine (inter-band) between AWS and 700MHz C. Not support for Verizon's Cellular or PCS holdings.

Dish: Release 12 support to combine their S band (AWS4) spectrum (inter-band) with the 700 MHz E holdings. This is the only aggregation scenerio for the US that combines FDD operation (AWS4) with TDD operation (700MHz E).

In listening to the wireless carrier earnings calls for 4Q2012, many of the analysts are interested in the timing for offering VoLTE. VoLTE stands for Voice over LTE, in other words, Carrier VoIP. It is unclear whether the carriers are looking at this as a launch of a handset supporting only VoLTE or whether it is essentially a dual-mode handset providing VoLTE where the quality is acceptable and traditional 2G or 3G voice everywhere else.

There is no doubt that 4G speeds enable VoLTE and all of the other VoIP over-the-top (OTT) providers like Skype, OOMA, and GoogleTalk. Carriers will have the ability to better control their customer experience with their VoLTE service since they can change the QOS settings because they can identify the data as a voice call.

I believe that Verizon has essentially stamped a date for their networks being 100% VoLTE for voice as the same 2021 data for shutting down CDMA. This is a reason time frame for networks to mature so they are capable of supporting VoIP seamlessly across the carriers footprint.

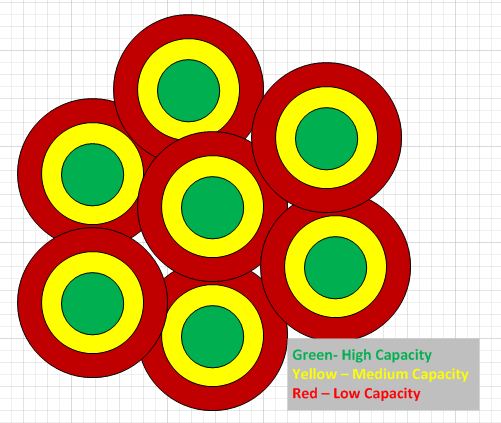

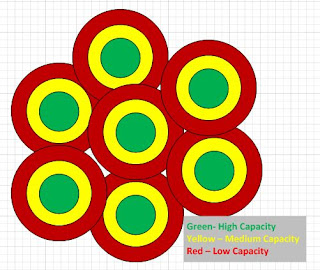

A key consideration that is not openly discussed, is the fact that the traditional wireless carriers that began as wireless voice providers have only overlaid their 4G data networks on top of a network that was originally designed for voice. This is important because capacity is impacted differently on a voice network than a data network. A voice user, whether 100ft or 4 miles from a site, essentially consumes the same amount of voice capacity. A data user, 100ft from the site, is capable of transmitting his data with a high efficient data modulation scheme, which reduces the capacity burden on the cell site. A user, 4 miles from the site, will receive his data using a more robust modulation scheme with a significant cost to the site's capacity. In this example the first user transmits his data on a train that has 64 cars for data, while the user 4 miles from the site only has 4 cars to carry his data.

How does this affect VoIP and the launch of VoLTE? With the diagram above I have indicated the areas of each cell site that will have high, medium, and low capacity based upon their voice network design. These are the areas that VoIP voice quality will suffer due to lack of coverage or capacity. With each carrier only offering LTE on one channel, the option to add additional spectrum to solve the capacity issue is not available. Carriers are pursuing small cell solutions to meet this capacity need but it will require extensive time to mature the networks to support VoLTE and VoIP on a standalone basis.

Posted during the 3GPP RAN Meeting on Dec 4-7, 2012 in Barcelona, Spain.

Customer Requirements for LTE Advanced Carrier Aggregation for Band 5 and Band 17. This appears to be supporting AT&T's need to aggregate carriers between their 700MHz (Band 17) and the Cellular band (Band 5). No mention of including the redefined WCS band. Could this be a sign that AT&T's growth plan for LTE will be to grow into the cellular spectrum first, and then to the WCS spectrum?

There were several interesting details that came out of the Deutsche Telekom Capital Markets Day 2012. The primary announcement concerned T-Mobile USA being blessed with the ability to sell the iPhone. T-Mobile's new CEO, John Legere indicated that it will have a dramatically different experience than the other iPhone on the market. In addition T-Mobile will sell it unsubsidized, although they will offer financing plans. This should continue to drive T-Mobile's Cost Per Gross Add (CPGA) down, although they didn't disclose if this only affects their iPhone retail business or potentially all of their retail. This is a dramatic step which eliminate the primary issue that I have had with the subsidy pricing model. I have a problem with paying the same monthly rate for my smartphone if I am out of contract as the guy that who just got a new device. With T-Mobile's plan the true cost of upgrading will be carried by the customer, with the expectation of lower monthly rates.

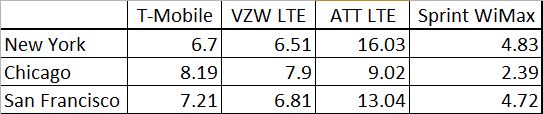

Above is a restatement of the testing data from PC Magazine which T-Mobile released. It is interesting to note how far their speeds have fallen from their early announcements in late 2010 concerning the HSPA+ network. It is also worth noting that they compared AT&T's LTE network. You can again see the loading effect on the network. AT&T's Chicago network was launched September 2011 so it has been loading for over a year reflecting the slower speeds. AT&T's complete New York and San Francisco networks are much newer, launching September 2012, thus carrying less traffic. I am curious why T-Mobile did not chose to compare themselves to AT&T's 4G (HSPA+) network.

From a LTE network build perspective, this was the first time I have heard clearly that T-Mobile is deploying tower top electronics. It is interesting that they state that they are the first carrier in North America to broadly deploy radio-integrated antennas. Clearwire was the first carrier to deploy tower top base stations, followed by Sprint with their Network Vision project. T-Mobile is playing up the fact that their radios are some how integrated into the antenna. Not really an earth shattering announcement. From a technology perspective, deploying the tower top base stations will fill in coverage holes and improve data speeds so it is a good move. In addition, these base stations will be Release 10 capable, meaning a software update will move these radio from the LTE features to the LTE Advance features.

The Numbers:

- Current 4G Network covers 225 million POPs

- Release 10 Equipment being deployed to 37,000 cell sites

- T-Mobile and MetroPCS: Migration not Integration

- With MetroPCS Spectrum Position across Top 25 service areas is improved by 21%

- Planning to shutdown 10,000 macro sites from MetroPCS

- Retain and integrate 1,000 MetroPCS sites

- Operating MetroPCS Markets

- San Francisco

- Detroit

- Boston

- New York

- Dallas

- Atlanta

- Florida (except panhandle)

- MetroPCS brand will increase coverage from 105MPOPs to more than 280MPOPs.