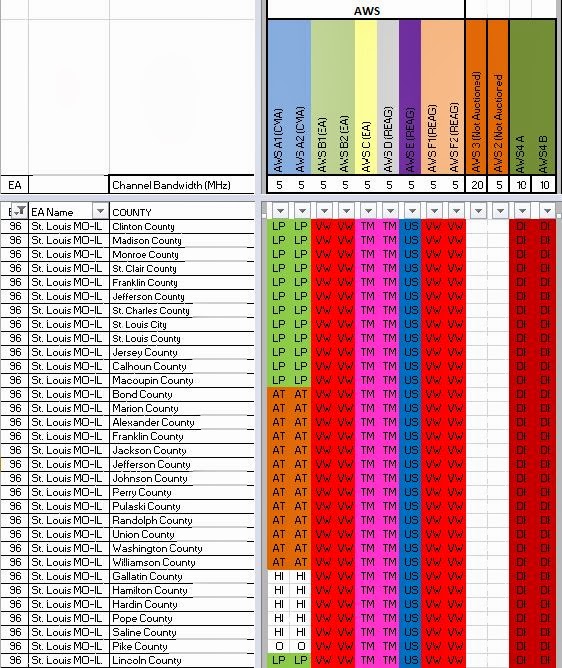

It is interesting to look at the details of Verizon's spectrum purchase from US Cellular in the St Louis market area (EA-96). Many industry sources talk about how purchase will provide 20MHz for Verizon's LTE. While this is true, it should not be confused with Verizon deploying a 20 x 20 channel. As can be seen from the Spectrum Grid view of AllNet Labs' Spectrum Ownership Analysis Tool, Verizon is purchasing the AWS B channel and previously owned the F channel. Although Verizon will own 20 MHz of spectrum, it is not contiguous and until they can deploy Release 12 software code into their network, they will have to operate this spectrum as two separate 10 MHz channels. Release 12 is likely a 2015 or maybe 2016 release since operators are either planning or deploying Release 10 currently.

The industry talks alot about Carrier Aggregation (CA) but there are several facts that are not well understood. First, Release 10 includes the functionality for carrier aggregation but the frequency band definitions for the US are not included until Release 11. Another point that needs to be understood is that the initial definitions require that aggregated carriers be in contiguous blocks in different spectrum bands (inter-band) or in separate blocks but in the same band (intra-band). For Release 11, only 2 carriers can be aggregated together. For Release 12, Verizon has sponsored a work group that will allow 3 carriers to be aggregated, 1 from the 700MHz band and 2 different carriers from the AWS band. Thus, Release 12 will be necessary for Verizon to aggregate their two AWS blocks of spectrum with their 700 MHz LTE.

The Spectrum Grid view is sorted by the EA geographical area which show that the AWS B and C licenses have not be dis-aggregated. The A channel licenses do show discontinuity since they were originally auctioned as CMA licenses. AT&T through their Leap purchase will strengthen their AWS ownership in this market.

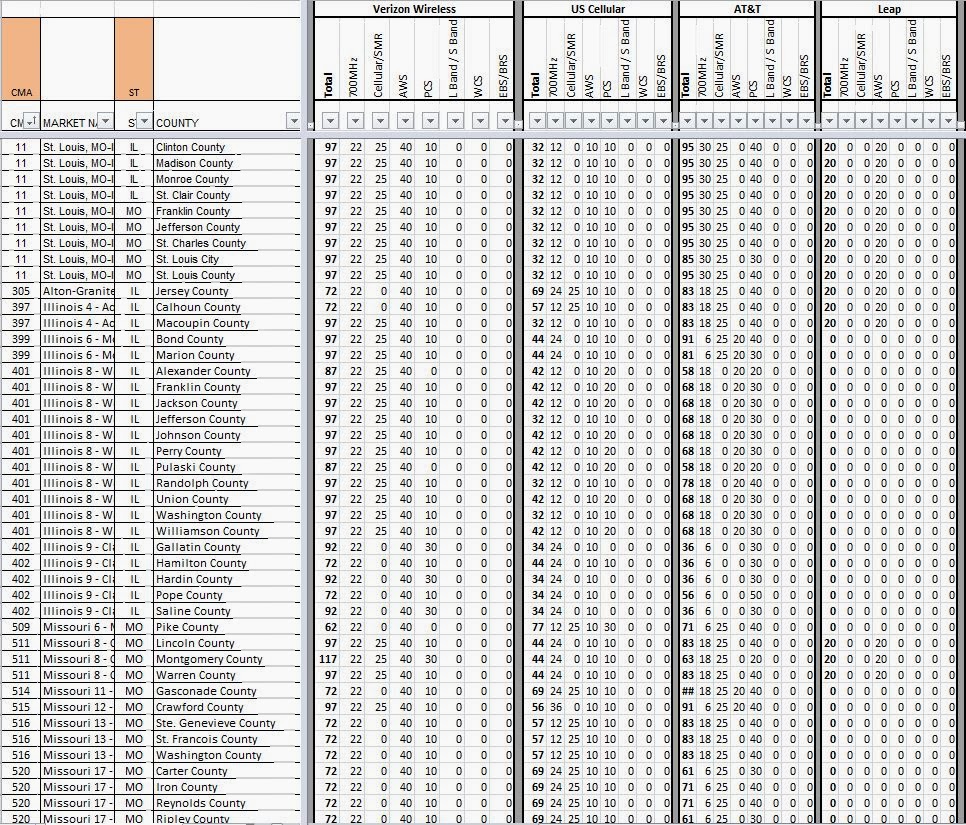

To look at the competitive picture for spectrum in the St Louis market (EA-96) we can look at the

Company By Band worksheet from the AllNet Labs' Spectrum Ownership Analysis Tool. Looking first at Verizon, we can see the variety of spectrum depths across the EA that Verizon indicated in their FCC filing. Verizon will range from 62 MHz to 117 MHz depending on the county. The only county that Verizon controls 117 MHz is Montgomery County, MO which is 40 miles west of St. Louis.

Looking at the other carriers in this market we see that US Cellular will still control between 32 MHz and 69 MHz, while AT&T with their Leap purchase will control between 61 MHz and 105 MHz.

T-Mobile controls between 40 MHz and 60 MHz with two counties at 70 MHz and Sprint with their Clearwire purchase controls between 130 MHz and 242 MHz.

Sprint completed the 2Q - 2013 earning call this morning providing a few details about their plans for Clearwire's 2.5 GHz spectrum.

Sprint intends to overlay all of the 38,000 cell sites with the 2.5 GHz spectrum. Clearwire has stated previously that 40% of their 16,000 sites are at the same towers as Sprint. Steve Elfman clearly stated that the 2.5 GHz network would have a higher cell density, guaranteeing that 2.5GHz only sites will be prevalent in Sprint's network.

Sprint has clearly signaled a return to the original Clearwire vision of a seamless, high capacity, high speed, wireless network.

Let's go through the site numbers:

1) Sprint expects 2000 sites supporting 2.5 GHz TDD-LTE this year. This was Clearwire's original commitment with the capacity hotspot mission. Clearwire had fairly firm plans to expand this site count to 5000 sites (hotspots).

2) 40% of Clearwire site (6,400) are located at the same tower as Sprint. Will Sprint move these sites onto their tower lease and back-haul? Saving the additional tower lease makes sense, but shifting the back-haul capacity from the "free" microwave back-haul, to Sprint's lease circuits would be adding a large and growing expense to Sprint's bottom line. A mis-understood fact on the wireless carrier back-haul is that although they will describe the back-haul as fiber back-haul with "unlimited bandwidth", the carriers are typically paying for bandwidth services delivered on fiber. This means, a 100 Mbps back-haul circuit is provided to the site on fiber for a cost based upon the back-haul capacity (100 Mbps). If Sprint added Clearwire's traffic to there existing back-haul, they would have to double or triple the capacity, probably doubling their overall back-haul expense.

Steve Elfman also made some interesting comments related to Sprint's 800 MHz spectrum (iDEN). He felt it was important to deploy for in-building penetration. I am still waiting to hear if there is a significant deployment of Sprint's 800 MHz spectrum in rural areas (with CDMA and LTE). If you look at the Virgin Mobile coverage maps, you can see the landmass covered by Sprint's network.

Expanses (non-green areas) in the West/Northwest and Southeast could utilize a Sprint 800 MHz greenfield build. I continue to believe that the primary benefit of lower band spectrum (600,700, Cellular) is coverage in less dense areas. I don't believe that there is a significant different building penetration improvement at the lower frequencies.

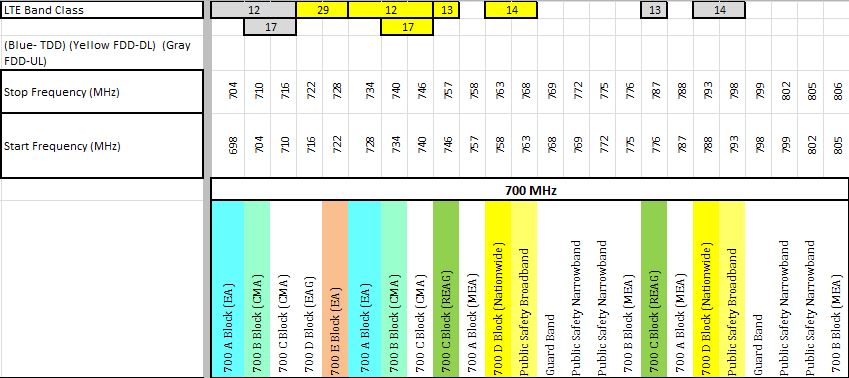

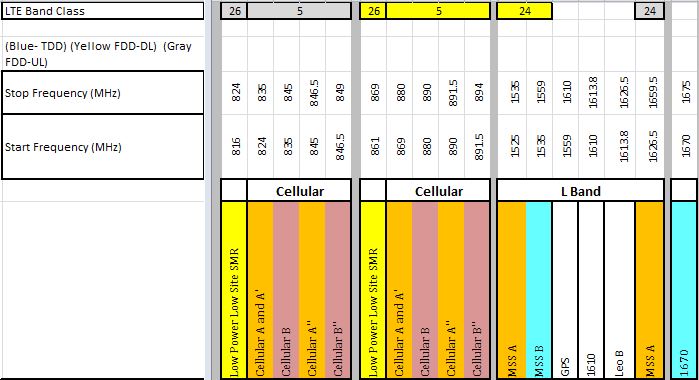

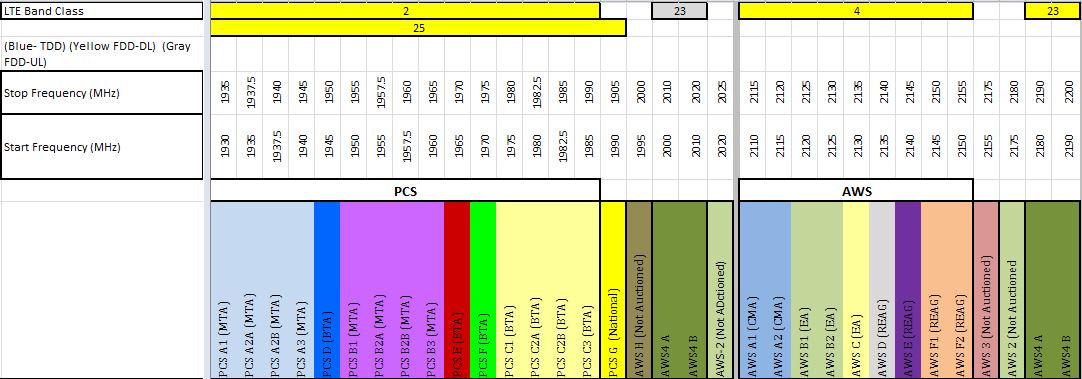

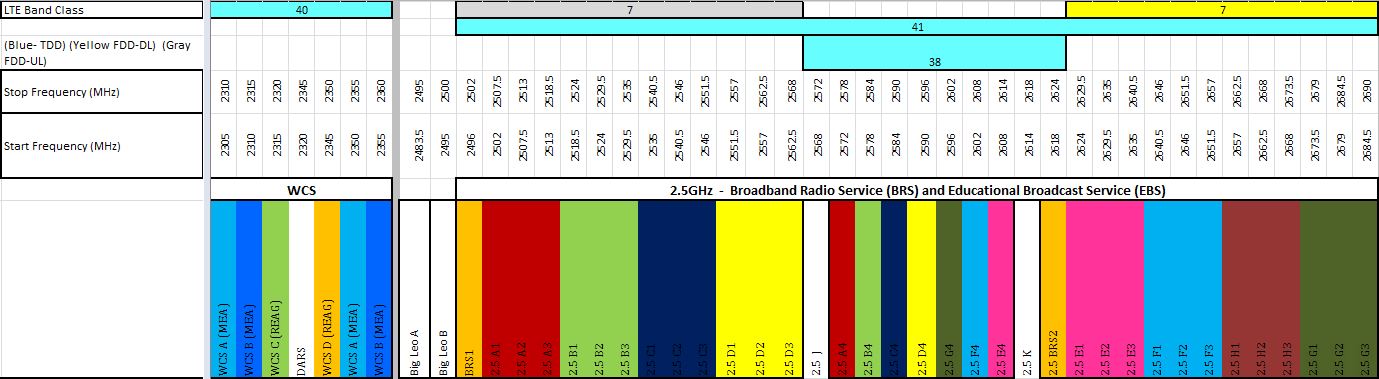

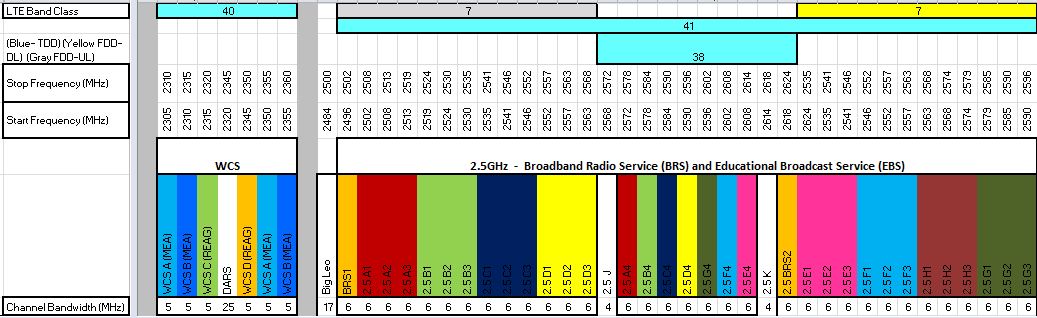

With AT&T's announcement that they are meeting some challenges related to testing operation between LTE Band Class 29 and Band Classes 2 and 4, I figured that many readers would appreciate a reference map for how these band classes relate to the US mobile radio and satellite spectrum bands.

All of these screenshots are from the AllNet Labs Spectrum Ownership Analysis Tool, where we display and provide analysis tools related to spectrum ownership for all of the US mobile radio and satellite spectrum bands for all 50 states and US territories.

AllNet Labs Spectrum Ownership Analysis ToolIn the images below, the band classes are color coded Gray for Uplink Spectrum, Yellow for Downlink Spectrum, and Blue for Spectrum supporting Time Division Duplex.

700MHz Spectrum

SMR/Cellular/L-Band Spectrum

AWS/PCS Spectrum - Uplink

PCS/AWS Spectrum - Downlink

WCS/EBS/BRS Spectrum

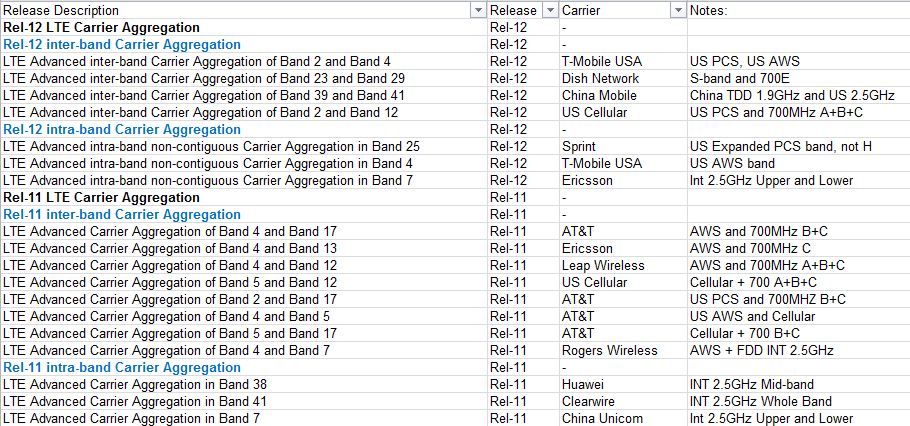

Recently I reviewed the 3GPP Standards site to check in on the status of LTE Carrier Aggregation. I found a gold mine of information.

First a few definitions: Carrier Aggregation allows a wireless carrier to band together different blocks of their spectrum to form a larger pipe for LTE. This can be accomplished in two ways: Inter-band and Intra-band.

Inter-band combines spectrum from two different bands. The spectrum in each band to be combined must be contiguous within that band. Intra-band combines spectrum from two non-contiguous areas of the same band.

Here is a link to an article from 3GPP that explains Carrier Aggregation.Below is a table summarizing the relevant 3GPP working group descriptions for Carrier Aggregation.

First of all, the current network release for all carriers is Release 9. T-Mobile, Sprint, and Clearwire have announced that they are deploying Release 9 equipment that is software up-gradable to Release 10 (LTE Advance). From the chart, it does not appear that there are any carrier configurations planned until Release 11. Release 10 appears to be a late 2013 commercial appearance and Release 11 will likely be very late 2014 or mid-2015. For Carrier Aggregation to work it must be enabled and configured at the cell site base station and a compatible handset must be available. The handsets will transmit and receive their LTE data on two different spectrum bands for the Inter-band solution. All handsets currently only operate in one mode, 700MHz, Cellular, PCS, AWS, or 2.5GHz.

Highlights by Carrier:

Canada: Rogers Wireless will have support for inter-band aggregation between their AWS spectrum and the paired blocks of 2.5GHz spectrum.

AT&T: Inter-band support in Release 11 for their Cellular and 700MHz spectrum, inter-band support to combine their AWS and Cellular spectrum, as well as configuration to support combining their PCS and 700MHz spectrum. All of the 700MHz band plans only include their 700B/C holdings. No 700MHz inter-operability.

USCellular: Inter-band support in Release 11 for Cellular and 700MHz (A/B/C). No support for PCS or AWS spectrum combinations

Clearwire: Intra-band support for the entire 2.5GHz band. China Mobile is also supporting this with an inter-band aggregation between 2.5GHz and their TDD 1.9GHz spectrum.

Sprint: Support in Release 12 for combining (intra-band)their holding across the PCS spectrum, including their G spectrum but not the un-auctioned H spectrum. No band support for their iDEN band or the 2.5GHz band.

T-Mobile: Support in Release 12 for intra-band in the AWS band and inter-band between AWS and PCS.

Verizon: Ericsson appears to be supporting Verizon's need to combine (inter-band) between AWS and 700MHz C. Not support for Verizon's Cellular or PCS holdings.

Dish: Release 12 support to combine their S band (AWS4) spectrum (inter-band) with the 700 MHz E holdings. This is the only aggregation scenerio for the US that combines FDD operation (AWS4) with TDD operation (700MHz E).

In listening to the wireless carrier earnings calls for 4Q2012, many of the analysts are interested in the timing for offering VoLTE. VoLTE stands for Voice over LTE, in other words, Carrier VoIP. It is unclear whether the carriers are looking at this as a launch of a handset supporting only VoLTE or whether it is essentially a dual-mode handset providing VoLTE where the quality is acceptable and traditional 2G or 3G voice everywhere else.

There is no doubt that 4G speeds enable VoLTE and all of the other VoIP over-the-top (OTT) providers like Skype, OOMA, and GoogleTalk. Carriers will have the ability to better control their customer experience with their VoLTE service since they can change the QOS settings because they can identify the data as a voice call.

I believe that Verizon has essentially stamped a date for their networks being 100% VoLTE for voice as the same 2021 data for shutting down CDMA. This is a reason time frame for networks to mature so they are capable of supporting VoIP seamlessly across the carriers footprint.

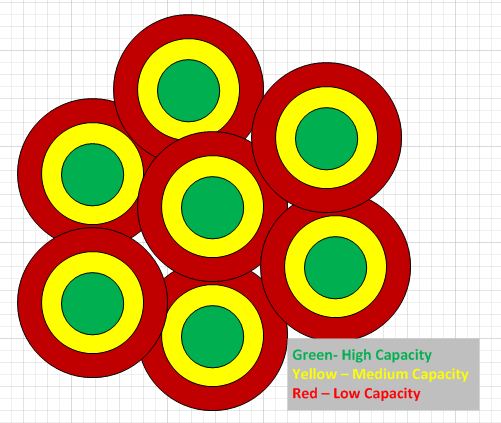

A key consideration that is not openly discussed, is the fact that the traditional wireless carriers that began as wireless voice providers have only overlaid their 4G data networks on top of a network that was originally designed for voice. This is important because capacity is impacted differently on a voice network than a data network. A voice user, whether 100ft or 4 miles from a site, essentially consumes the same amount of voice capacity. A data user, 100ft from the site, is capable of transmitting his data with a high efficient data modulation scheme, which reduces the capacity burden on the cell site. A user, 4 miles from the site, will receive his data using a more robust modulation scheme with a significant cost to the site's capacity. In this example the first user transmits his data on a train that has 64 cars for data, while the user 4 miles from the site only has 4 cars to carry his data.

How does this affect VoIP and the launch of VoLTE? With the diagram above I have indicated the areas of each cell site that will have high, medium, and low capacity based upon their voice network design. These are the areas that VoIP voice quality will suffer due to lack of coverage or capacity. With each carrier only offering LTE on one channel, the option to add additional spectrum to solve the capacity issue is not available. Carriers are pursuing small cell solutions to meet this capacity need but it will require extensive time to mature the networks to support VoLTE and VoIP on a standalone basis.

Globalstar's Proposed Terrestrial Low-Power Service (TLPS) has some well thought-out approaches. Globalstar has petitioned the FCC to allow them to utilize their 2484-2500 MHz "Big Leo" satellite spectrum to provide terrestrial coverage.

Globalstar's spectrum lies directly above the 2.4GHz ISM band which hosts a vast majority of the WiFi in use today, as well as bluetooth and microwave ovens. Directly above the Globalstar spectrum is the EBS/BRS spectrum controlled primarily by Clearwire.

Globalstar has proposed terrestrial operation on a the newly named AWS5 band. It would essentially be a 4th non-overlapping WiFi channel (Channels 1,6,and 11 are the primary non-overlapping WiFi channels). It would still be a 22MHz wide channel, using the ISM band above Channel 11 (which is lightly used) and about 10MHz of their AWS5 channel. Globalstar believes that most existing WiFi devices could support this spectrum with a over-the-air software updates so a massive number of devices could be overloaded to this network once it is constructed.

Also intriguing is the improved performance characteristics of this spectrum. First, since it is licensed to Globalstar, they can control the use of the spectrum. They envision a carrier grade network using this spectrum that would manage Hotspot power levels and interference. Since this spectrum has much less interference, it is capable of covering larger areas with higher speeds than typical WiFi.

If Globalstar can figure out the backhaul aspect to providing this service, I think they will have a leg up on other white-glove WiFi service providers since they are better able to manage the RF environment for their frequencies. It is conceivable that Globalstar would host WiFi overloading for all of the 4 national carriers. I still see the biggest challenge to be in a residential environment where they envision a hotspot in my house being under their control, but likely on my cable internet service. I'm pretty sure Comcast won't react well to my residential internet service supporting a commercial operation.

Is this a service that could be considered or expanded into the EBS/BRS channels that are adjacent to Globalstar's spectrum? The answer is yes. Clearwire has stated that they have excess spectrum. I would anticipate that this would look like a private LTE network on Clearwire's spectrum versus WiFi on Globalstar's, but it would not be as feasible as Globalstar's proposal due to the current lack of devices that support LTE on the EBS/BRS frequencies.

Below is a link to an Investor's Presentation provided by AllNet Labs detailing the licensing, geographic, and leased versus owned challenges of Clearwire's Spectrum.Audio and Slide PresentationPresentation Outline

Agenda- History of the EBS/BRS Spectrum

- Owned versus Leased Spectrum

- LTE Band Configuration

- Recent Auctions

- Substantial Service

- Issues before the FCC

- Spectrum Sale Challenges

Another area of interest from the Sprint / Clearwire conference call yesterday were Erik Prusch's comments related to Clearwire's attempts to sell spectrum in 2010. Erik indicated that the offers they received were below value.

I will be conducting a webinar for GLG Research on January 4, 2013 where I will be discussing the history and challenges of Educational Broadcast Service (EBS) and Broadband Radio Service (BRS) spectrum. I believe that the undervalue offers were due to issues with the spectrum channelization, geographic boundaries, unlicensed channels, and FCC mandated obligations for leased spectrum.

Inevitable. If you have followed the Sprint/Clearwire saga since they were joined with Google, Time Warner, Brighthouse, Comcast, and Intel; it was obvious that Clearwire had a hard road ahead. In yesterday's announcement Erik Prusch indicated the depth of the internal concern; Clearwire had retained an advisor to provide options for restructuring.

Once the carrier consolidation of 2012 occurred, the only path forward I saw for Clearwire was funding minimal operations into the 2014 time frame, with a hope that the other 3 national players would finally need the wholesale access to Clearwire's spectrum. With each of the national players, except Sprint, lining up their LTE capacity growth spectrum, the need for wholesale access to Clearwire's WiMax or planned TDD-LTE network was unnecessary. Clearly Sprint needed Clearwire for its LTE growth spectrum and at $0.21/MHzPOP I believe we will look back 5 years from now and view this was steal. Not only has Sprint put in concrete their LTE capacity growth, but they have cornered the market available spectrum for years to come. When you consider that Clearwire controlled 160MHz of spectrum which could be expanded to nearly 200MHz in most metro areas with additional spectrum leasing and spectrum purchases, Sprint has the only meaninful swatch of "new" spectrum that will come to market in the next 5 years.

I don't see the Broadband Incentive auction, the Dish spectrum, or the recent 3.5GHz spectrum as meaningful for efficient macro network coverage. Those subjects are covered in other blogs.

The purchase of Clearwire does not guarantee smooth sailing for Sprint. Sprint still has very significant short term issues. Their LTE network is 5X5 which is the smallest of any of the national carriers. In addition, their customers with WiMax devices will continue to transition over to this network as they upgrade their devices. Clearwire's TDD-LTE hotspot network is only at the construction start stage, with likely very limited coverage throughout 2013. Clearwire has talked historically about devices arriving for this network 2Q or 3Q 2013. Thus, there won't be any material movement of traffic from Sprint 3G or LTE network until early 2014. From what I experience on my Sprint Samsung S3, the 3G network is already challenged and LTE is not available in my market (Seattle). It will get worse before it gets better.

When Clearwire first offered wholesale access to its spectrum, it was using the WiMax technology. It had built this technology in the 2.5GHz band and it was covering up to 80 markets by the end of 2010. At this time Clearwire provided meaningful WiMax coverage in each of their markets for Sprint, Comcast, Time Warner, and Best Buy to provide their customers 4G Only WiMax devices. Essentially, Clearwire's WiMax network had broad enough coverage that these operators could selectively offer their customers service in the markets that Clearwire offered WiMax service.

As Clearwire has embarked on the TDD-LTE strategy, their wholesale model has gotten a bit more complex. First, they continue to sign up relatively small partners for their WiMax wholesale offering: Simplexity, Freedom Pop, Best Buy, CBeyond, Mitel, NetZero, Locus, and Kajeet. They have Sprint already signed for Wholesale Access to the forthcoming TDD-LTE network and added Leap to the WiMax partner list early in 2012.

Leap demonstrates the change of direction for wholesale agreements for the TDD-LTE network. For their TDD-LTE roaming strategy, a roaming partner would need a "thin" LTE network providing coverage in their markets. They would then roam over to the Clearwire TDD-LTE "hot spots" only for capacity. Sprint's 5x5MHz FDD-LTE deployment would qualify as a "thin" LTE deployment. This implicit requirement for a "thin" coverage network, eliminates non-carriers from the TDD-LTE wholesale process since it would be difficult to sell "spots" of coverage across Los Angeles if you didn't have service already over the area.

In addition, the quantity of sites in the Clearwire LTE plan started at 8,000 of their 16,000 sites, was reduced to 5,000 sites and recently has arrived at 2,000 sites. This has increased the challenge of finding wholesale partners with this very limited coverage.

The idea of Clearwire hosting Dish's AWS2 spectrum seems to be bouncing around the news pages today. Clearly (no pun intended), Clearwire operates a 4G network that is very similar to Sprint Network Vision concept. With the necessary zoning and permitting, Clearwire could add this spectrum band with a new set of antennas and tower top base stations. So, this would get Dish to market after they pass the standard's body requirements for defining the new band, but what does it provide Clearwire. Different than Sprint, they don't need the spectrum, they need capital to increase the TDD-LTE build out. I believe that Clearwire would much rather Dish sign up for their wholesale mobile broadband service with an infusion of capital. My next blog will look at one of the other drawbacks for potential wholesale partners like Dish with Clearwire's TDD-LTE plan. Check back later in the week.

Clearly the wireless industry has locked in spectrum pricing with the MHz-POP pricing model, but is this the right way to look at it as we move into a 4G World where data throughput and capacity are key? For those that aren't familiar, the typical value of spectrum is determined by the $/MHzPOP which is the dollars spent for the spectrum divided by the total amount of spectrum times population that spectrum covers. This model falls short now as carriers are interested in acquiring larger contiguous blocks of spectrum enabling higher users speeds and more capacity.

To use a real estate analogue, a large plot of land is much for flexible for multiple uses, than two plots, even if they are in the same neighborhood. In real estate, the developer that is able to consolidate several tracks of land into a larger development is rewarded as he sells the larger development.

In the wireless industry, we continue to price based upon the $/MHz POP basis, even as carriers such as T-Mobile and Clearwire have combined adjacent channels to create larger bands of spectrum to utilize in larger LTE channels. T-Mobile has worked this year with Verizon, SpectrumCo, and MetroPCS which will allow it to assimilate a 2X20MHz LTE channel on a national basis. Clearwire has leased and purchased operators in the BRS and EBS spectrum bands providing it with an average of 160MHz of spectrum in the top markets. Since Clearwire's spectrum has many geographical boundaries, it is difficult to say how many 20MHz channels they could support across each of their markets, but they have been successful consolidating small bands of spectrum into larger more flexible spectrum bands.

How does a larger band of spectrum affect the wireless carriers? In the US, carriers have deployed FDD-LTE in 1.25MHz channels, 5MHz channels, and 10MHz channels. As you increase the channel size throughput performance improves because a lower percentage of the data packets are dedicated to overhead activities Qualcomm has provided achievable LTE Peak Data Rates for different channel bandwidths based upon whether the antennas are 2x2 or 4x4 MIMO.

Link to Qualcomm DocumentAs you can see in the 4x4 MIMO downlink case, the throughput is 12Mbps greater in the 20MHz channel than the composite of 4-5MHz channels.

So if a 20MHz channel is 4% more efficient than 4 - 5MHz channels should the MHz POPs pricing adjust accordingly?

By the way.. I am going to look for more source data on the capacity improvements for wider channels, a 4% improvement would seem to be relatively negligible. I recall hearing 30% improvements in capacity when a channel size is doubled, but I haven't been able to re-source that data for this blog. More to come.